My daughter texted my wife and me about the tariffs. I didn’t have the heart to crush her spirits—that the $200 for deodorant, some kitchen knives, soap, paper towels—yeah, that’s been the price point since late into the pandemic.

If I remember my high school American history and American government courses correctly, how tariffs were explained to me was that you put a tariff on a product, the price of that product goes up in the grocery store, and therefore, you as a consumer, in theory, would choose the equivalent American product instead of the foreign-made whatchmacallit.

That’s all fine and good until you realize a ton of stuff in the U.S. we don’t make anymore. But we’re looking at more big-ticket items increasing in price right now as opposed to, say, my daughter’s paper towels and bar of soap. Washer and dryers, TVs, kitchenware, computers, cell phones, cars. Anything with a large amount of aluminum or steel. But we will be seeing higher food prices this month. Think bananas, coffee, fish, beer, canned tomatoes, Reddi-wip.1

We’re staring down the loss of real money for 2025, approximately $2,400 per household.2 That’s like a whole mortgage payment.3

My wife has recently cut down on her coffee intake, which has been, by the way, a boon to me. I can buy less and drink more. My favorite coffee shop has smartly and preemptively switched to smaller mug sizes charged at the same price—albeit, you can get a “free” refill. Probably a lot of people don’t. They’re now losing money on me, I’m sure.

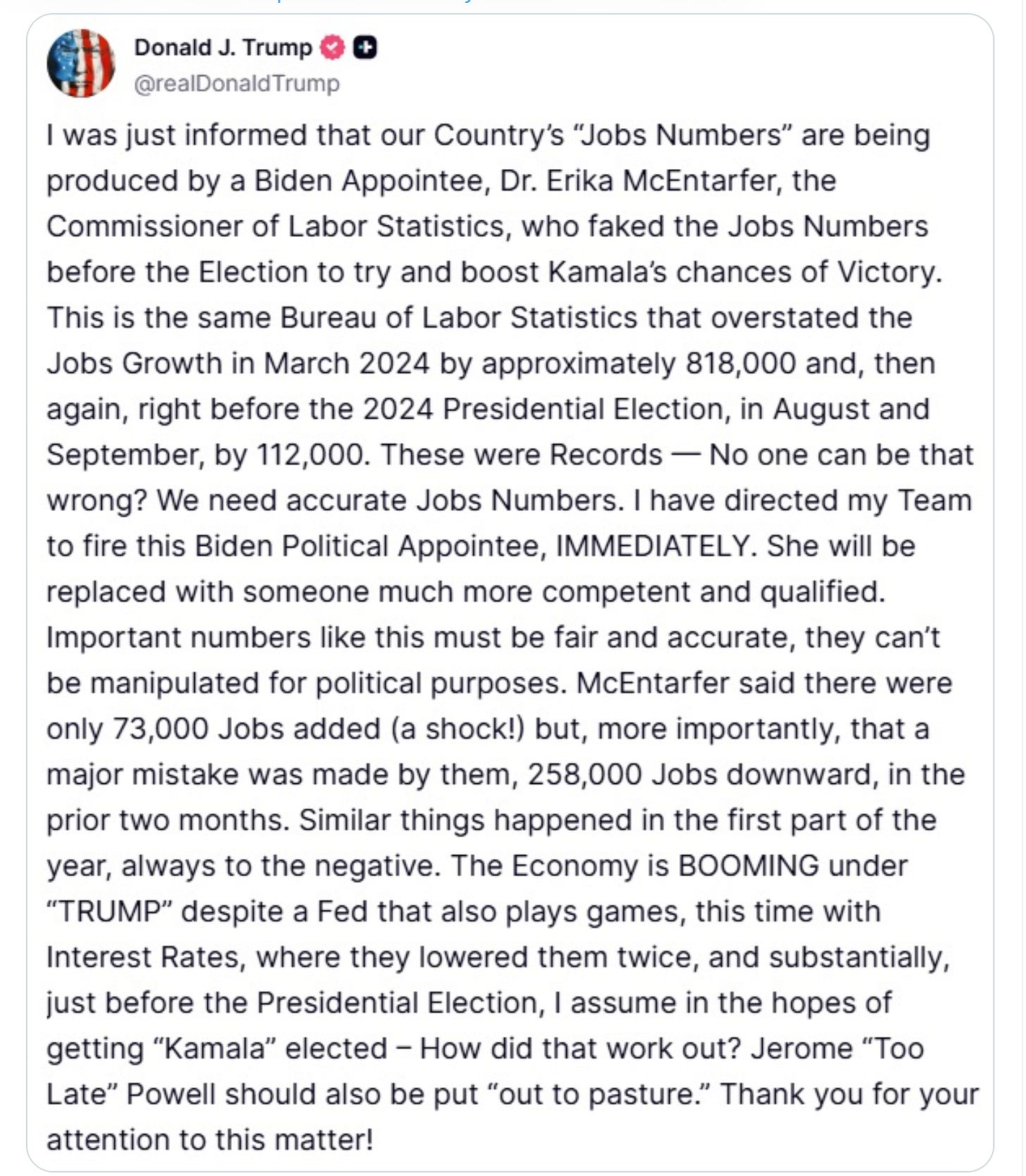

And according to CBS News Money Watch, the tariffs are set to drive another round of inflation.4 And then we are served the labor statistics.

Payrolls rose by just 73,000—falling far short of expectations—while job numbers for May and June were revised downward by a combined 258,000, revealing a much steeper slowdown than previously reported. The unemployment rate ticked up to 4.2% from 4.1%, and weakening household employment further underscored the labor market’s fragility.5

Those numbers seem esoteric until you look at what it means for the average joe. Imagine your neighbor just spent $700 on a new washer and dryer thinking they were catching a July sale. But the price was quietly inflated because of steel tariffs and slowed factory output. Meanwhile, her kid just graduated and is struggling to find any job, let alone one with benefits. Across the street, the guy who does DoorDash part-time (wait, that’s me) just lost one of his shifts because demand dropped—people aren’t tipping as much, and the algorithm knows but just doesn’t care either.

And Trump’s response is: let’s fire the dudette who gathers the data.

This isn’t some far-off Wall Street drama. It’s the slow, quiet contraction that turns your neighbor’s side hustle into her main job, and forces your favorite coffee shop to switch to smaller mugs with a smile and a “free refill” policy.

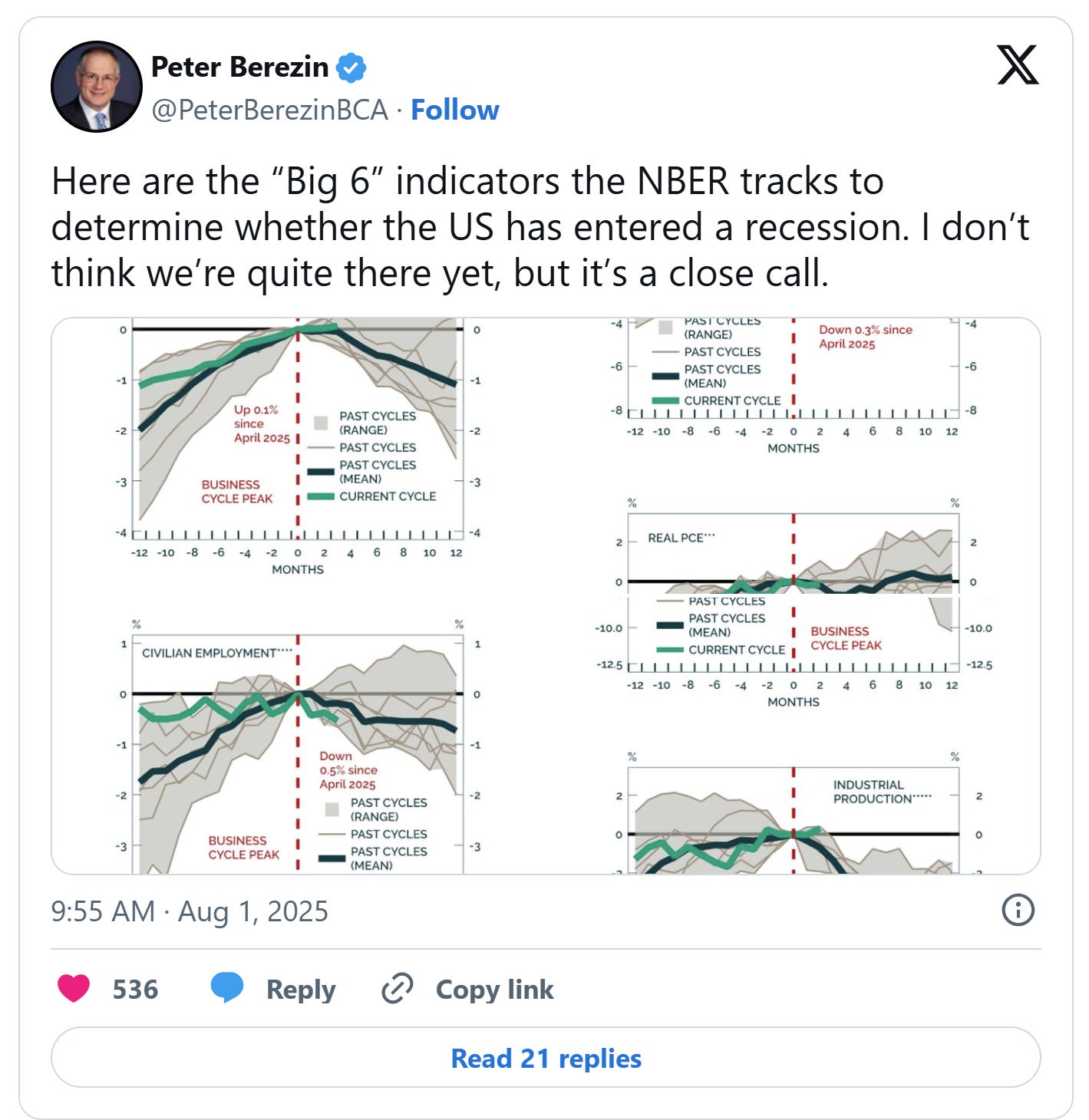

And so then you’re broke before you even notice. And on top of all that, maybe we start looking at a recession.

Beth Hammack, president and CEO of the Federal Reserve Bank of Cleveland, stated that low-income families are already facing financial challenges. “I hear individuals trading down, they go to the supermarket and they can’t buy ground beef. They’re buying hot dogs, they’re looking at their $400 emergency fund, and it’s not able to pay for a new air conditioner or the car repairs that it used to be able to pay for,” she told CBS.

But according to personal Finance Expert Nischa Shah, nearly 60% of the American population doesn’t know what an emergency fund is because they don’t have one.

So What the Hell Do You Do?

1. Know the Leak

You don’t need a budget spreadsheet. You need a gut check. Where is your money actually going? Not where you wish it went. Not where it used to go. Track one week. Cash, card, coffee, cat food—track it. The leak usually isn’t rent. It’s death by 7,000 tiny charges. You can’t fix what you don’t face.

2. Outlearn the Market

This economy rewards people who adapt faster than it changes. If your side hustle isn’t cutting it anymore, learn a new hustle. Free digital courses. YouTube university. Hell, get paid to try something: test UGC, flip stuff on Marketplace, learn basic automation tasks. If AI’s gonna take jobs, you might as well ride shotgun.

3. Cut What You Don’t Love

Subscription bloat is real. If you’re going to be broke anyway, at least be broke doing things you care about. Keep the Spotify. Ditch the meal kit. Keep the gym. Ditch the bullshit “self-care” box. Starve your apathy so your ambition has a shot.

4. Barter > Beg

If you can’t afford help, trade for it. Babysit for a haircut. Cook for a car repair. Build an economy around you that doesn’t require cash to function. That’s not soft. That’s how communities survive collapse.

5. Find Your Leverage

Even broke, you’ve got currency. Influence, reputation, labor, time, proximity, insight. If you can write, speak, sell, build, or solve—you’ve got something worth trading. Don’t ask for help like you’re a burden. Offer help like you’re the badass that you know you are.

6. Don’t Play the Game You’re Being Sold

You don’t need to win the economy. You just need to opt out of the dumb parts: the brand loyalty, the fake urgency, the belief that if you’re struggling, it’s your fault. It’s not.