HousingWireHousingWire

Today, we woke up to former President Trump as our newly elected president and a Republican Senate. What does this mean for housing? First and foremost, mortgage rates have shot up today on the news. Now, let’s look at the probability of them going higher or lower in the future.

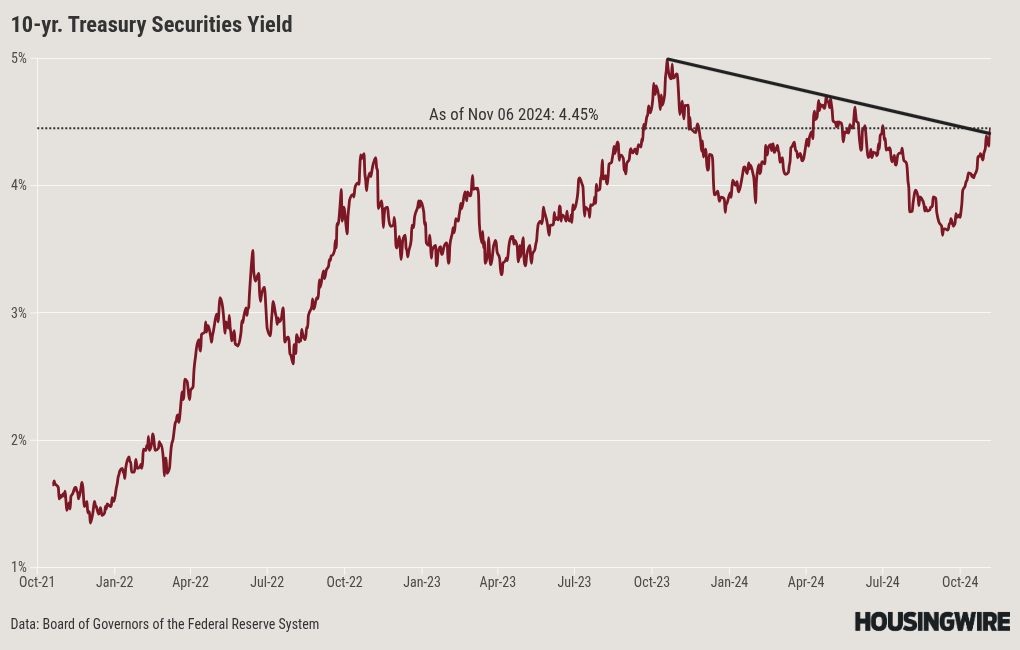

Last night on my Instagram reel, I called the election very early — as soon as the 10-year yield touched 4.41%, since that was my trigger yield. As I am writing this today, the 10-year yield is 4.45%. My line in the sand has been 4.40%; if we close above this level and get follow-through bond selling, mortgage rates can go higher. But I am going to wait until the end of this week to assess this because of the volatility in the markets right now.

Many Wall Street conservatives have said a Trump victory would mean higher mortgage rates due to bigger deficits, more inflation from tariffs and a less dovish Federal Reserve. Is their logic sound, or are they talking about their own trades?

We’ll be discussing this topic in greater detail tomorrow in the HousingWire Daily podcast. For now, some key points:

The Federal Reserve

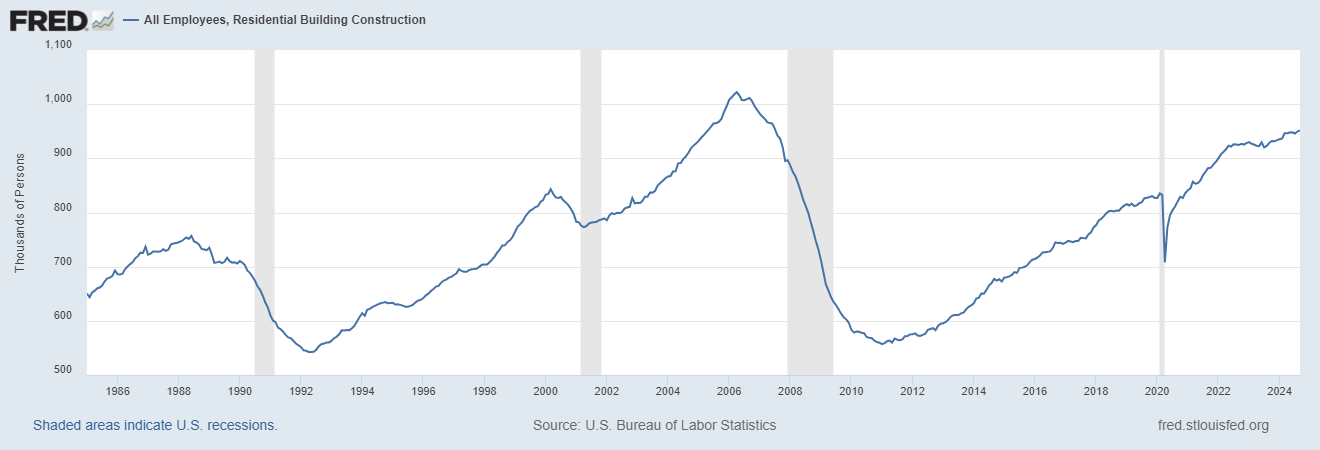

In 2018, the Fed wrote a paper about tariffs and the possible inflation they could cause; they concluded that hiking rates to fight tariff inflation would lead to a recession. This puts their dual mandate at risk, so fighting a one-time price adjustment wouldn’t be in their interest. Also, when rates rose recently, this put the housing construction labor at more risk. Losing jobs for residential construction workers is crucial in my economic cycle work: In any recessionary data line, mortgage rates go down in that scenario.

Residential construction workers: Gray bars are periods of recessions

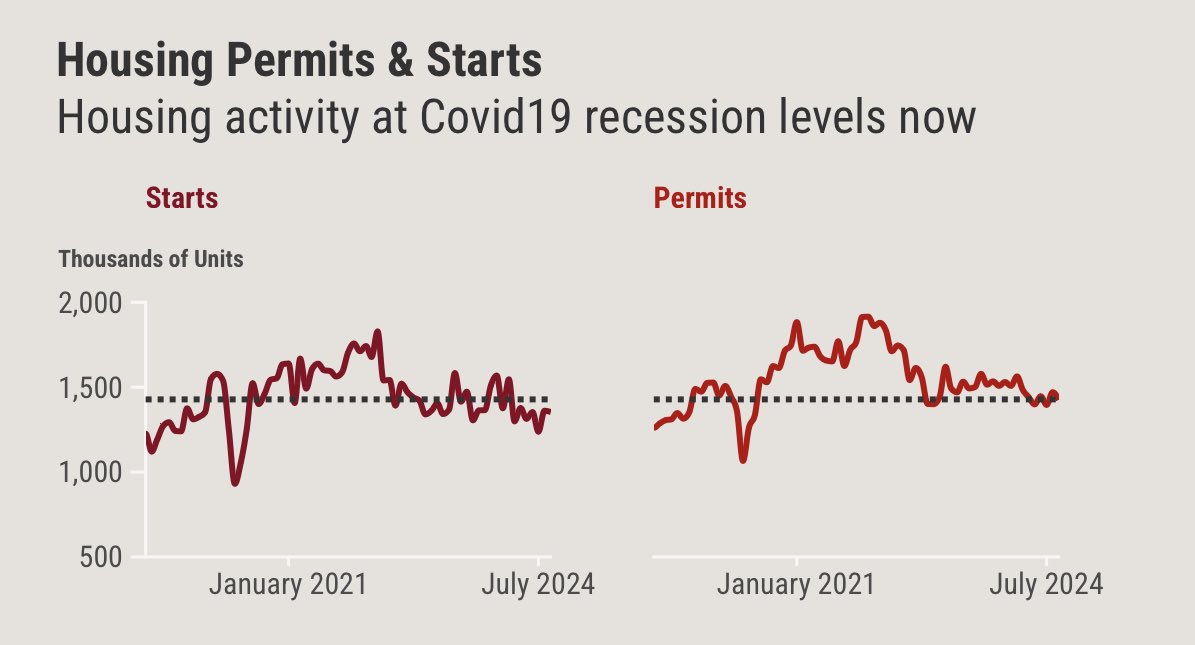

When mortgage rates were 6.75%-7.50%, there was no growth in residential construction workers, and currently, housing starts and permits are at recessionary levels. When mortgage rates fell toward 6% and the builder’s confidence picked up, sales grew. So, we have limits on how long we can keep mortgage rates elevated before we start to lose construction workers. The Fed pays attention to that because that is part of their dual mandate — something to think about as we go forward.

Manufacturing growth and lower deficits

If President Trump wants to grow manufacturing exports, create more manufacturing jobs and keep the economy afloat, he needs a few things:

- The dollar needs to get weaker so we can export more stuff out of the country.

- He also needs rates to go down. He can’t afford housing construction to go into a recession at this stage. Also, he plans to tackle the deficit due to interest payment level falling by lower Fed Fund rates.

To provide affordable housing, you either need lower rates or a lot more building than what we are doing now. I discussed this reality in the HousingWire podcast today and I wrote about manufacturing in December 2016, focusing on the realities of what can happen with manufacturing.

Trade war tariffs

A lot of conservative Wall Street types have said we’ll get higher rates because of a trade war that will happen if Trump begins his term with 20% tariffs.

One thing to remember is that Trump didn’t initiate the trade war tap dance with China until 2018 — two years after he took office — and waited until the tax cuts were in place. Back then, it created a lot of market drama and business investment stalled out because companies didn’t know what would happen. So, be skeptical here about an open trade war happening right away.

What I describe above are the conditions that will temper mortgage rates staying elevated for a long period because President Trump needs lower rates and a weaker dollar, and he can’t afford to have housing construction go into a recession if it wants to attack affordable housing. This is a complex subject, so I will go into more detail in our podcast out tomorrow. However, keep these key bullet points in mind when thinking about Trump and higher mortgage rates.