HousingWireHousingWire

“The standard of living of the average American has to decline,” he said. “I don’t think you can escape that.” These were the words of Federal Reserve Chairman Paul Volcker as he testified before Congress in October 1979. Inflation was 13%. Volcker’s predecessors, Arthur Burns and William Miller, had failed to control prices. Stagflation gripped the United States. We were in an economic death spiral.

Volcker would go on to raise the Fed Funds Rate to 20% in 1981, forcing the country into a deep recession. The 30-year fixed hit 18% in October of the same year and unemployment surpassed 10% shortly thereafter. The standard of living for the average American had indeed declined.

But by 1986, inflation was defeated (1.9%), mortgage rates fell to 10%, and the Beastie Boys released “License to Ill.” At the time, I cared about one of these things. By 1988, unemployment had a 5-handle, and I was graduating high school. The most painful economic period in modern U.S. history was concluding. Volcker’s tough call worked.

History is full of tough calls.

In WW2, the Brits cracked Hitler’s Enigma machine and learned of the Luftwaffe bombing planned for Coventry, England. Churchill allowed for the city’s demise to preserve his secret upper hand. The Enigma codebreaking was a crucial factor in the Allied victory over Germany in WW2.

Jacinda Ardern was Prime Minister of New Zealand when the pandemic began. She immediately locked down the entire country in March of 2020, issuing a “Stay at Home to Save Lives” directive. The economic & social backlash was fierce. For the entirety of the pandemic, New Zealand’s death rate from Covid was 0.086%, lowest in the world. The United States’ death rate was four times higher.

Via climactic event (pandemic), significant policy misstep (transitory inflation), and irresponsible deficit spending, today’s Federal Reserve finds itself in “tough call” territory.

The Fed recently slashed the Fed Funds rate for the third time this cycle while simultaneously announcing that inflation would not reach the goal of 2% until 2027. The Dow Jones dropped 1,100 points on the day and the 10-year yield increased by the widest margin on any Fed Day since 2013.

But first, some economic data

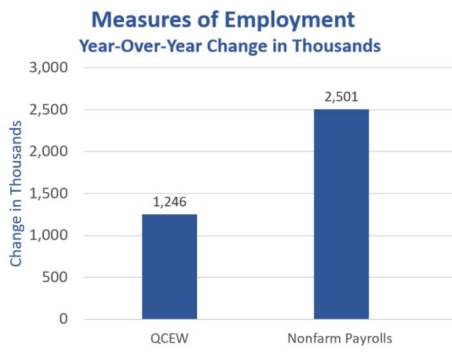

I assert that reporting from our Bureau of Labor Statistics (BLS) is masking a far weaker set of current economic conditions. Exhibit A: November’s QCEW report. While the monthly Nonfarm Payroll (NFP) number gets all the pub regarding job creation, the QCEW is the “behind-the-scenes” gold standard. The Quarterly Census of Employment and Wages captures 95% of jobs with a sample size of 12.2 million establishments. The NFP is a survey of only 629,000 establishments with a response rate of 43%. The NFP has signaled a surprisingly resilient labor market for the past 2 years. The chart below reflects mortgage-backed securities overlaid with monthly nonfarm payroll numbers for 2024. Note how MBS perform when NFP job creation is reported as robust. Of all economic reports affecting mortgage rates, this one is the big kahuna.

In November of this year, the far more robust and accurate QCEW effectively audited nonfarm payroll job creation from Q2 of 2023 to the same period in 2024. When the BLS reconciles these figures in early 2025 and they are made official, prepare for a ~1 million subtraction of full-time jobs. Remember this past August when the BLS subtracted 818,000 jobs from Q1 2023 to the same period in ‘24? That wasn’t a one-off.

Chart courtesy of Mishtalk.com.

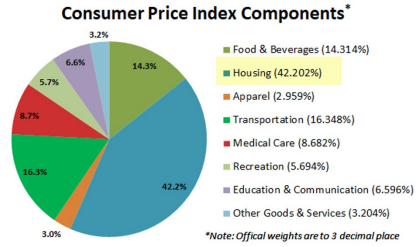

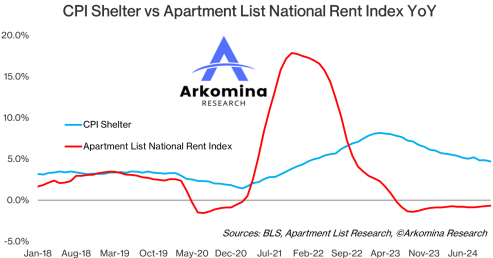

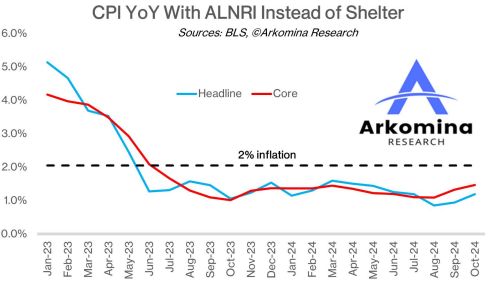

Exhibit B: Meanwhile, the BLS is reporting shelter inflation using metrics with extreme lag and subjective surveys that inflate the overall inflation number. Shelter/Housing is the single largest component of CPI. A bad quarterback on a good team can tank the season. Shelter can impact CPI like no other in the basket of goods.

Substitute a more data-driven method of aggregating rents, such as the Apartment List National Rent Index, and you will find inflation is already below 2%. Charts by Arkomina research.

So, if the economic data is flawed at best or manipulated at worst, aren’t Fed rate cuts appropriate? If conditions are actually weaker than we think, shouldn’t the Fed be less restrictive?

No. Allow me to explain.

Flawed thinking

Jerome Powell and his team are trying to win an unwinnable contest. They have embraced the “soft landing” narrative but have forgotten how to truly pilot. They are acting like politicians, playing not to lose instead of doing what it takes to win.

This is their dilemma:

Option A:

• Keep the FFR high.

• Ensure inflation is defeated.

• Endure the ire of the President-Elect and the nation.

• Risk higher unemployment and unnecessary recession.

Option B:

• Cut the FFR, declaring progress on inflation.

• Issue hawkish messages to avoid market exuberance.

• Attempt to steer the economy back to pre-pandemic conditions.

• Risk reigniting inflation and restarting a painful rate-hike cycle.

The Fed has chosen option B. It is the wrong choice.

To be clear, I am no Nostradamus. I’m the guy who invested his life savings in Webvan when he was twenty-seven. But I understand the bond market, and I need only observe its reaction to see the forest.

What the bond market is telling us

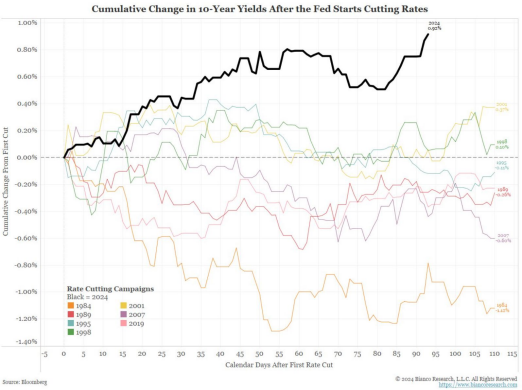

Below is a chart of the cumulative change in the 10-year Treasury from the beginning of every Fed rate cut cycle since 1989, courtesy of Bianco Research. The trajectory of the 10-Year since September 18th is historic and a flat-out rejection of the Fed’s actions. In other words, the market isn’t buying what Jay and team are selling.

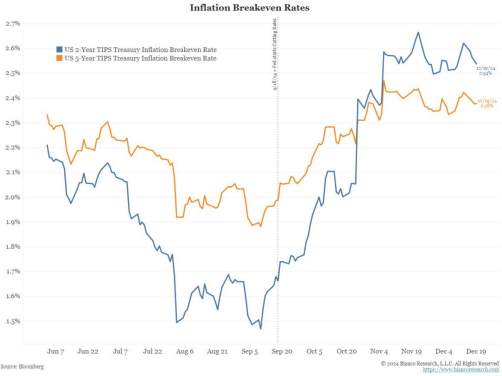

The second chart represents the 2-and 5-Year TIPS. Treasury Inflation-Protected Securities are designed to repay principal and interest of a bond investment but are adjusted to CPI. This helps mitigate inflation risk from devaluing the investment, a common concern with bonds. The hashed vertical line is September 18th, the day the Fed began cutting the FFR. The market’s expectations of 2-and 5-year inflation have done nothing but rise since Jay and Team began cutting. The market believes Jerome Powell is risking becoming Arthur Burns. If they are right, it may take Volcker-esque pain to fix this mistake.

Is the bond market perennially correct regarding the trajectory of inflation? No. Is it correct this time? Maybe.

Does it matter if the bond market is right or wrong now? No.

We’ve proven it is far easier for the Fed to stimulate our economy than slow it. Assuming the odds of throwing an economic bullseye are miniscule, to which side of this board should we err?

The bond market’s rejection of the current Fed option leads to two of my favorite topics. Risk & Math

The risk of option A is recession and rising unemployment. For every 1% increase in unemployment, an additional 1.7 million people will lose their jobs. Job loss is brutal, and it is not my intent to turn something devastating into an equation. If you are one of the affected, your unemployment rate is 100%. But these are the tough calls one must accept if he or she wishes to be Fed Chair. The downside of option A is another 1.7, or 3.4 or 5.1 million Americans will lose their jobs. At 5.1 million, the unemployment rate would be north of 7%. But inflation will be defeated.

The risk of option B is inflation reignites. This is what the bond market has already begun to price and why long-term yields are rising. Inflation affects all of us. We have 130 million households, which hold

337 million Americans. A 2023 survey conducted by Payroll.org estimates that 78% of Americans live paycheck to paycheck. A comparable study by Forbes Advisor revealed a similar number at 70%. This same number of respondents have less than $2,000 in savings. A repeat rise of inflation for this group,

which represents more than 90 million households means deeper credit card use, crippling debt, mortgage defaults, student loan nonpayment, automobile repos, bankruptcies, and a decision between groceries or rent.

The risk of option A is to sacrifice Coventry to win the war.

The risk of option B is the entirety of England.

This may be a tough call, but it is Not. Even. Close.

Conclusion

The Fed must choose the lesser of two dreadful things. The Fed needs to listen to the bond market and cease playing politician. Scrap the “soft landing” flight plan and remember there are passengers in the back counting on their discernment. Not their legacy.

Leaders make tough calls.

Back to Paul Volcker in 1979, sitting in front of Congress, completing his testimony: “We face unpleasant economic circumstances, and none of our choices is risk-free or pain-free. The time has come to deal with them.”

Mark Milam is the president and founder of Highland Mortgage.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.

To contact the editor responsible for this piece: zeb@hwmedia.com.